Who Is Building Europe's Unicorns?

The MBA is out. The technical founder is in: tracking the new DNA of European startups.

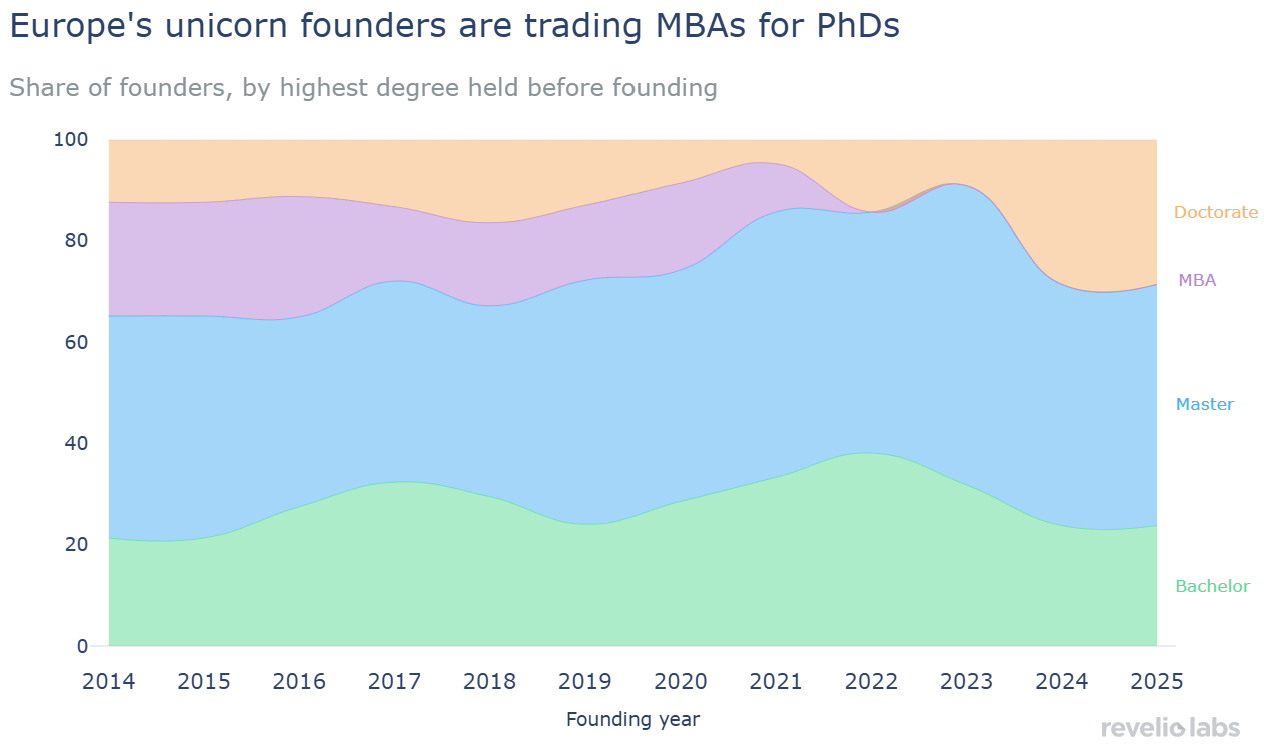

It takes a different person to grow a billion dollar startup today than 10 years ago. The typical profile of a recent unicorn founder is more experienced and more technical. Founders have longer pre-founding careers and are more likely to hold advanced technical degrees. Almost one-third of founders from the 2024-2025 cohort have a PhD degree relative to 10-15% in earlier cohorts. MBA prevalence, on the other hand, has significantly declined as none of the most recent founders hold an MBA.

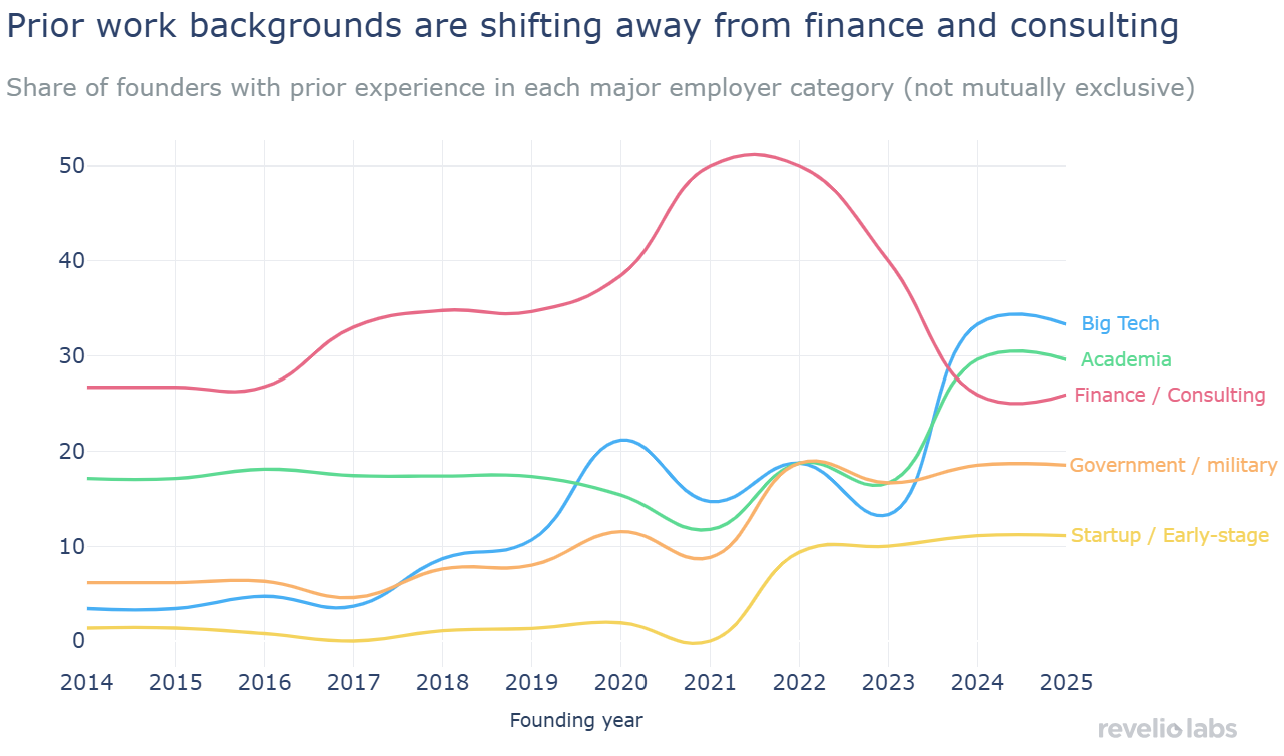

The founder pipeline is shifting away from finance and consulting and toward Big Tech and academia. After peaking at roughly 50% around 2021–2022, the share of founders with finance/consulting experience has fallen to about 25% in 2024–2025. Over the same period, Big Tech and academia have risen to roughly 30–35%, both now surpassing finance/consulting as founder backgrounds.

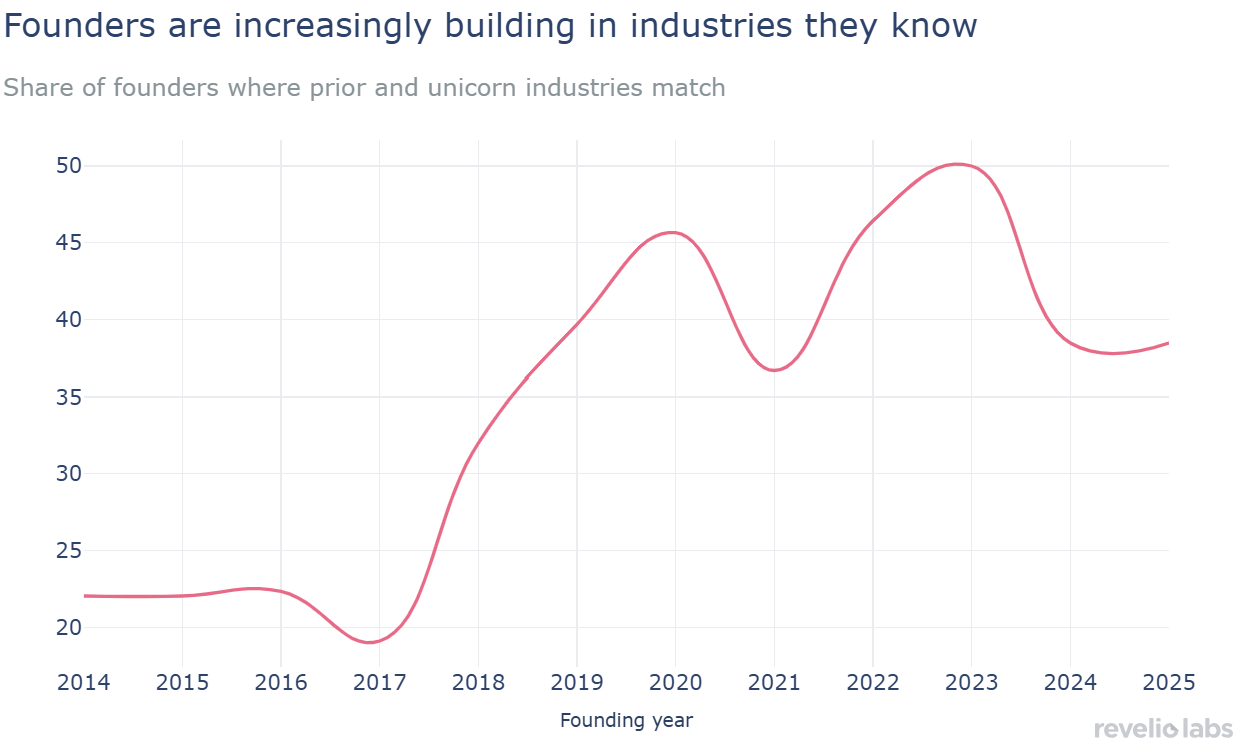

Europe’s unicorn founders are also more likely to found companies in industries where they already have direct experience. The share of founders whose prior employer industry matches their unicorn’s industry has risen from the low-20% range in the mid-2010s to around 40% in the most recent years.

Sign up for our newsletter

Our weekly data driven newsletter provides in-depth analysis of workforce trends and news, delivered straight to your inbox!

From fintech names like Monzo, Revolut, and Trade Republic, to AI and deeptech companies like ElevenLabs, Hugging Face, and Mistral AI, Europe’s unicorn ecosystem now spans a much broader set of sectors than it did a decade ago. Revelio Labs partnered with Accel to analyze what this shift looks like from the founder side.

The analysis covers 290 European unicorn companies. To build the dataset, we matched an extended founder roster with Revelio Labs’ individual profile data, allowing us to capture founders’ pre-founding work histories and educational backgrounds. Using European unicorns as a case study, the goal is to look upstream of valuations and funding rounds and ask a more structural question: who is now building billion-dollar companies?

This matters for two reasons. First, Europe is becoming a more competitive node in the global labor market. Second, the world’s startup market overall is changing. The last cycle was shaped by fintech, marketplaces, and software platforms. The current wave is increasingly tied to AI, deeptech, cybersecurity, defense, climate, and infrastructure. As a result, the data shows that founder archetype is becoming more experienced, more technical, and more closely linked to the industries founders previously worked in.

Do European Unicorn Founders Have More Experience Than Before?

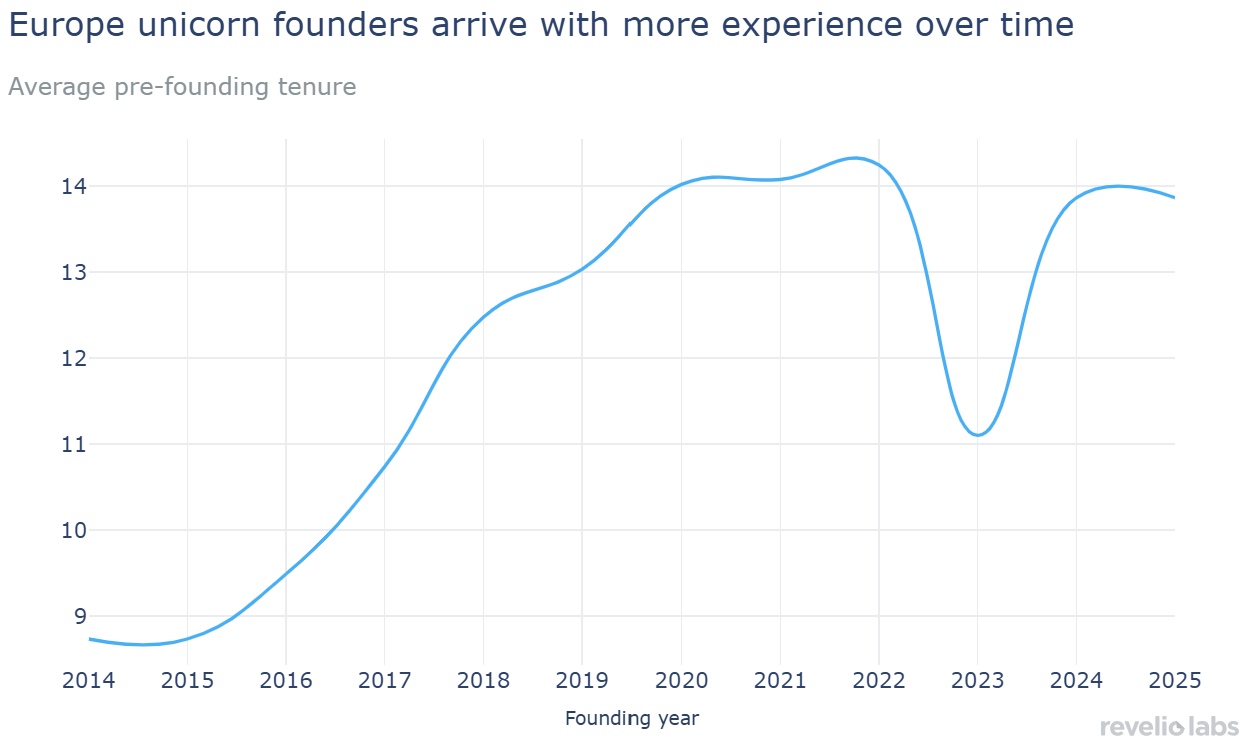

European unicorn founders are arriving with more work experience than earlier cohorts. Average pre-founding tenure rises from roughly 9 years for companies founded in the mid-2010s to roughly 13 years for the most recent founding years, peaking above 14 years for the 2020–2022 cohort. The dip around 2023 reflects a thin recent cohort and is mostly driven by SheMed, a women’s health company and a rare case of very young founders reaching unicorn status within a year of founding, a pattern almost absent in the rest of the sample. The overall trend challenges the classic image of the very young founder building straight out of school, mirroring a broader shift toward older, more experienced leaders. Europe’s newer unicorns are more often built by experienced operators who have spent years accumulating technical, commercial, or industry-specific knowledge before founding. That experience likely matters more in the current market. AI, defense, energy, cybersecurity, and infrastructure companies often require deeper expertise at inception than earlier consumer internet or marketplace domains. In this environment, a founder’s prior career becomes part of the company’s starting advantage.

Are Unicorn Founders Getting More Technical Degrees?

The education mix is also shifting. Master’s degrees remain the largest share of highest pre-founding credentials across most founding years, while MBAs have become less prominent in the most recent years. Doctorate holders account for a larger share than they did in the 2010s. The report also shows this clearly at the company level, where cohorts are defined by when companies became unicorns rather than when they were founded. The share of companies with a doctoral founder doubled from 9% pre-2023 to 18% among 2023+ unicorns, while MBA prevalence fell from 16% to 8%. The story is not just that founders are more educated. It is that the type of education associated with unicorn formation is changing. The newest cohort looks less MBA-led and more technically credentialed, consistent with a startup market increasingly shaped by AI, deeptech, cybersecurity, and applied engineering.

What Backgrounds do Europe's Unicorn Founders Have?

Another visible shift is in prior work background. Finance and consulting were dominant feeders for earlier unicorn founders, but their share has been falling sharply in recent cohorts. At the same time, Big Tech and academia have become much more prominent. This is exactly what we would expect from a more technical unicorn cycle. Finance and consulting experience were highly relevant for fintech, marketplaces, and business-model innovation. But AI labs, infrastructure companies, cybersecurity startups, and defense technology firms must draw from different talent pools. The newest founder pipeline is therefore less concentrated in traditional prestige industries and more connected to frontier technology, research institutions, government-adjacent work, and prior startup experience. Finance and consulting remain relevant, but they are no longer the defining background of the newest European unicorn founders.

European Founders Are Building Unicorns in Industries They Have Experience In

Recent founders are also more likely to build in industries that match their most recent pre-founding work. The share of founders whose prior employer industry matches their unicorn’s industry moves from the low-20% range in the mid-2010s to the high-30% range in the most recent years, after peaking around 2023. This suggests that European unicorn formation is becoming more domain-specific. We see in the data that Information Technology Services and Digital Commerce Services together account for nearly 39% of founders’ most recent pre-founding industries, making technical and digitally native backgrounds the clearest feeder base for Europe’s unicorn ecosystem. The next-largest single category, Financial Services, follows at just 14.1%. Media and Entertainment, Education Services, and Healthcare and Wellness Services also appear among the top feeder industries, showing that the founder pipeline now extends well beyond the traditional finance, consulting, and SaaS archetypes. Founders are not just leaving high-status feeder jobs to start companies in any attractive category. Instead, they are now more often building companies that extend directly from the industries where they already have expertise. That fits the broader pattern: more experience, more technical credentials, and more specialized prior work. Europe’s next unicorns are increasingly being built by founders converting accumulated industry knowledge into venture-scale companies.

Europe’s unicorn founder archetype is changing and that shift speaks to a broader evolution in the startup ecosystem. In Europe, the newest unicorn founders are more experienced, more technically trained, and more likely to emerge from technology and academia. For investors, this means founder sourcing has to broaden. The next breakout companies may not come only from repeat founders, finance, consulting, or elite MBA networks. They may come from AI labs, hyperscalers, research universities, defense organizations, energy firms, healthcare systems, and technical teams inside large enterprises. Europe is the case study here, but the lesson is broader: unicorn creation is becoming less about generalized entrepreneurial ambition and more about converting deep technical and industry knowledge into venture-scale companies.