Not All Data Centers Are Created Equal

Two distinct business models are creating very different community outcomes

Two business models for data centers, hyperscale operators and colocation operators, have emerged over the last 3 years. While hyperscale operators like Amazon and Google develop data centers for their own technology businesses, colocation operators lease out and maintain their computing infrastructure for clients, employing more people locally in the process.

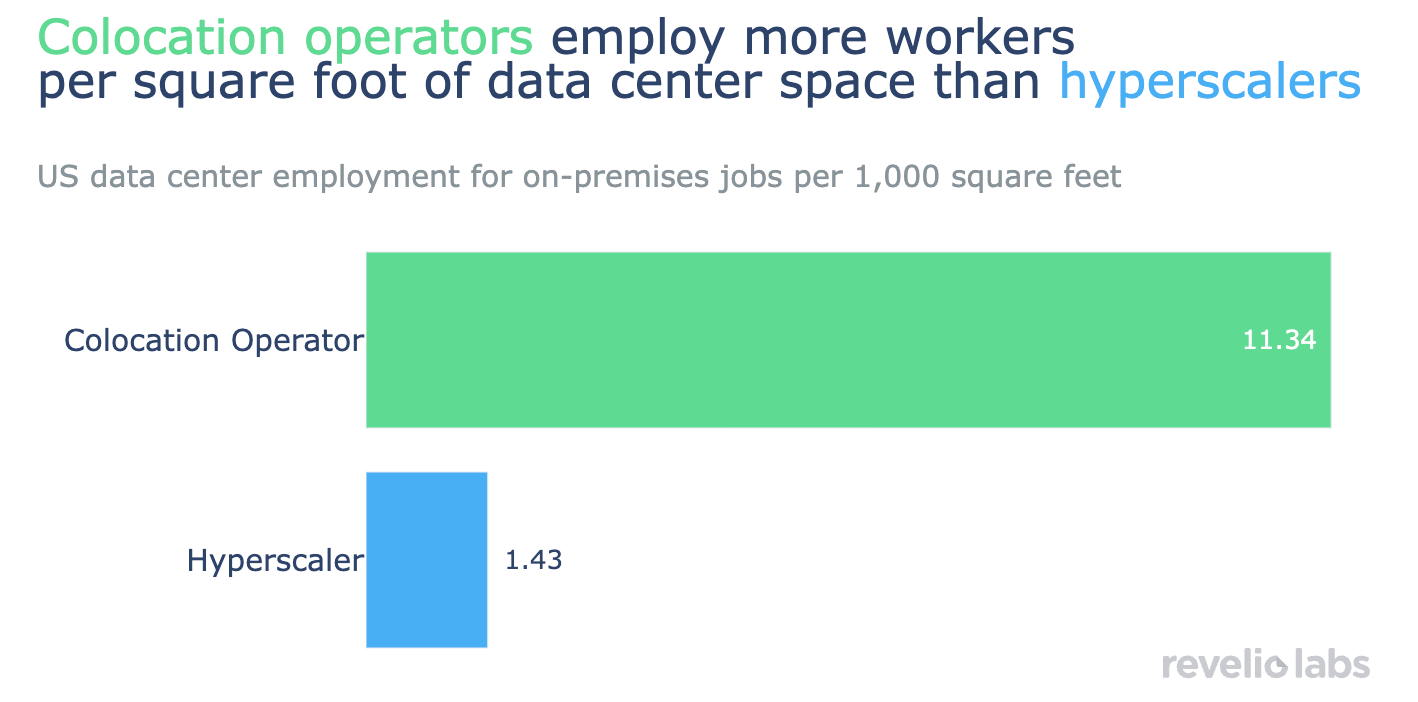

Considering how much space data centers take up, colocation operators appear to provide a higher return in terms of jobs created for the local labor market, employing more than ten times as many people per square foot compared to hyperscalers.

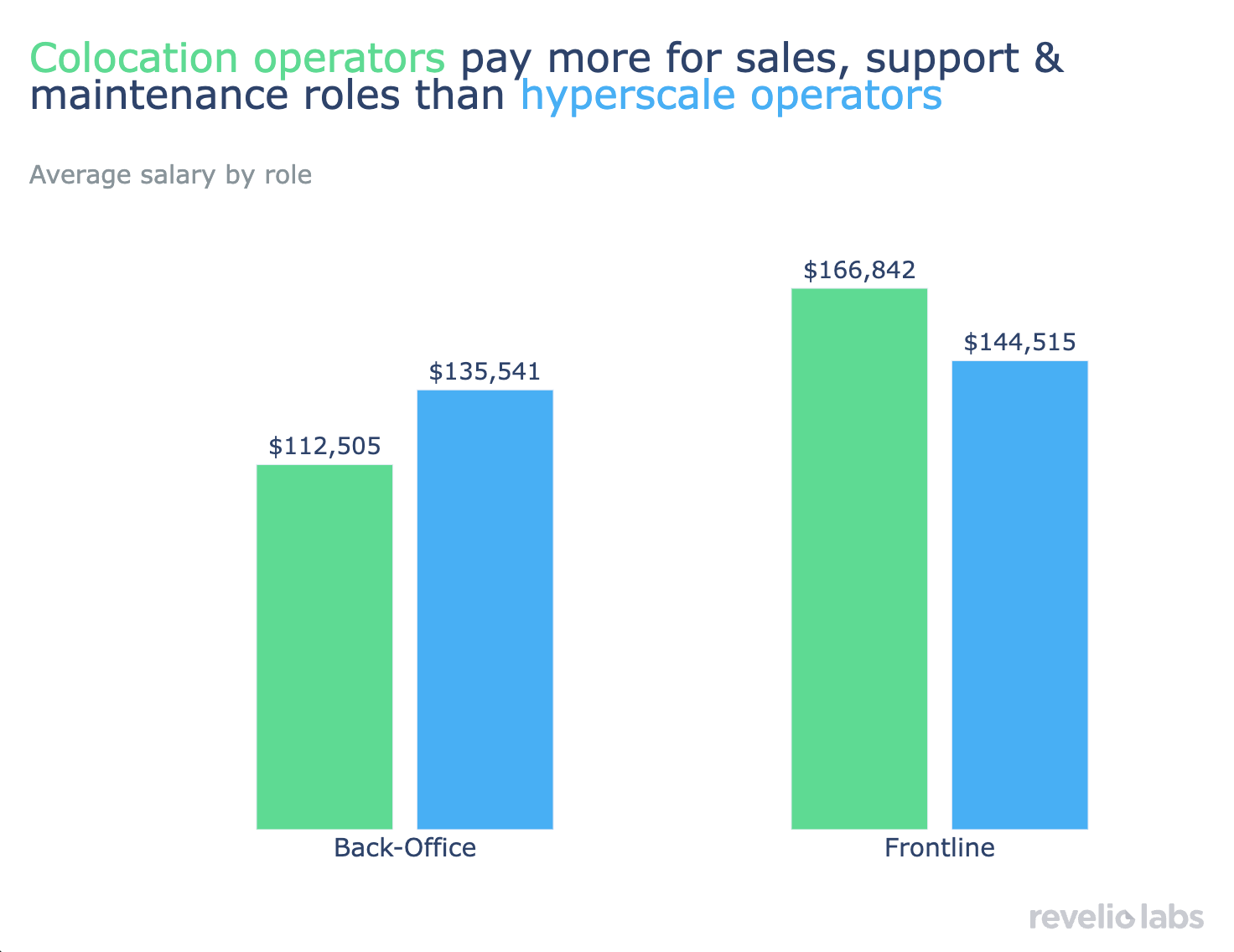

Colocation operators depend on client interactions and success, requiring more sales and customer-support as well as technical maintenance staff, all of which are jobs local communities are particularly well positioned to fill. Colocation operators also pay more for maintenance, sales, and support roles than hyperscalers, further benefitting the local labor force.

Sign up for our newsletter

Our weekly data driven newsletter provides in-depth analysis of workforce trends and news, delivered straight to your inbox!

Data centers have become an increasingly visible part of economic life, not only through public discourse and the ever-increasing integration of digital technologies, but physically as well. In a recent newsletter, we explored how data centers are spreading the benefits of the AI boom beyond traditional tech hubs and how local communities can prepare their workforces accordingly. Now, we answer a different question using Revelio Labs data: How the business models of data center operators shape the kinds of jobs, labor market spillovers, and economic benefits local communities ultimately receive.

Currently, the data center operators propelling the AI-driven industry boom employ two business models: hyperscale or colocation. Hyperscale leverages vertical integration. The “hyperscalers” such as Amazon, Google, and Microsoft, develop and maintain their own data centers to support both their customer-facing cloud services as well as internal computing infrastructure, i.e., for training AI models. On the other hand, colocation focuses on renting out data center capacity to clients. While a hyperscale data center may have a single tenant (Amazon or Google, for example), a single colocation center can have hundreds of corporate tenants.

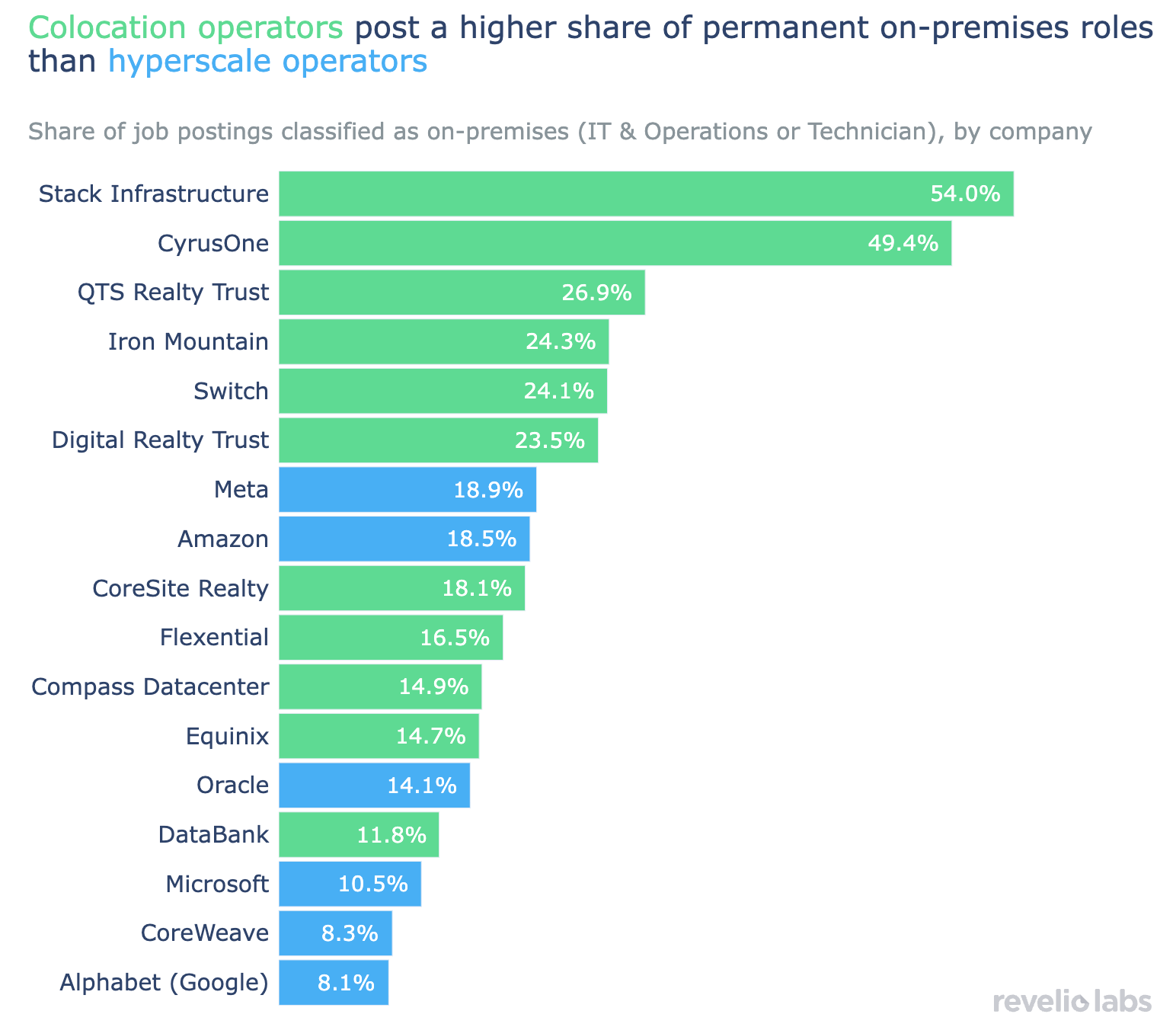

As we noted in our previous analysis, data center proposals can promise thousands of jobs, but most of these are construction-related and, therefore, temporary. The more important question for local communities is how many permanent jobs will a data center ultimately create? According to Revelio Labs data, it depends significantly on the business model. Colocation operators typically demand the permanent “on-premises” work, such as IT and technician jobs, that best aligns with local labor pools at higher rates than hyperscalers.

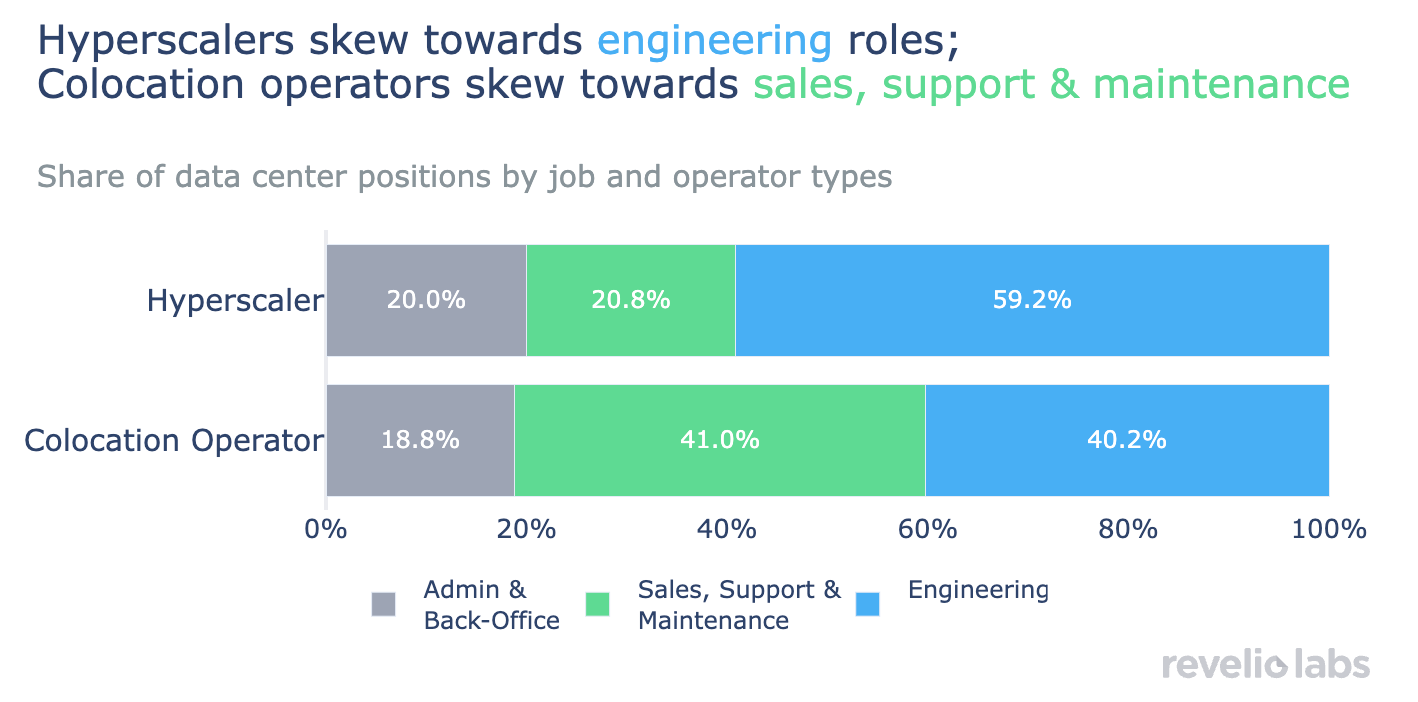

This discrepancy is closely associated with each company’s business model. Hyperscalers’ vertical-integration approach requires they not only build and operate data centers, but design, develop, and deploy cutting-edge software and hardware as well. As a result, almost 60% of their entire current workforce is engineers. The colocation model, however, is that of a service provider. It requires significant client-facing sales and customer support teams as well as IT and technician maintenance teams to attract and manage tenant clients and ensure their success.

What this means for communities considering data center opportunities is that an incoming operator’s model directly determines the degree of local employment the project is likely to generate. Skewing heavily towards engineering, hyperscaler workforces can operate remotely or from centralized headquarters rather than at the data center itself. Colocation operations, however, rely much more heavily on on-premises workers. In fact, this includes not only the IT and maintenance technicians to manage the equipment, but the sales and customer support professionals to handle the client-facing work as well.

As Revelio Labs data shows, colocation operators have a larger share of their employees in on-premises sales and customer support compared to hyperscalers (11% of employees at colocation compared to 0.8% for hyperscalers). This pattern is especially beneficial to many communities receiving data center projects since these roles require fewer specialized skills, which local labor supplies can adopt relatively easily. In other words, the colocation business model relies much more on local communities and their labor market.

We find that this closer alignment between the colocation model’s workforce needs and local communities’ labor supply is reflected in compensation as well. Colocation operators, while generally unable to compete with hyperscaler salaries, do in fact pay more on average for the frontline on-premises roles that are most critical to their operations as third-party data center service providers.

Beyond workforce composition, the operating model also determines the physical footprint a data center will impose on a community. Colocation operators typically manage campuses of around 100,000 square feet, while hyperscalers’ data centers can reach over 2.5 million square feet—the equivalent of less than two versus more than 40 football fields. Considering the strain that campuses can place on local environments, we measure the employment rates in terms of this footprint, per square foot occupied. We find that colocation operators employ far more workers per square foot than hyperscalers, suggesting that from a labor market perspective, they generate a greater economic return on the land they occupy.

At scale, these employment per square foot rates suggest that with over 700 data centers currently under construction, local communities across the US might ultimately expect to see anywhere between 700,000 and 2.5 million new on-premises jobs in total.

That said, the ultimate economic impact that a new data center will have on a local community depends on more than just the workforce the incoming operator’s business model requires. Hyperscalers and colocation operators differ in operational size and capital expenditures and present markedly different risk profiles as well. Where hyperscalers may offer greater operational scale through their vertical integration, colocation operators may provide greater stability through the diversification of their client portfolio. For communities considering receiving a data center, all of these factors matter, but the business model’s alignment with the local labor market is clearly a critical component to ensure lasting mutual benefit and success.