The Companies Spending the Most on AI Are Also Spending the Most on Humans

Ramp x Revelio Labs: new spending data shows heavy AI investors grow employment by over 10%, including entry-level hiring

Companies that adopt AI look very different from companies that never adopt. AI adopters are larger, more engineering-intensive, more likely to be venture-backed, and were already growing at a faster rate before adoption.

Companies that adopt AI tend to grow faster than companies that have not yet adopted it, but the relationship is driven almost entirely by high-intensity adopters. Companies making the largest AI investments grow employment by roughly 10% on average following adoption, while low-intensity adopters see no statistically significant change.

Among companies making the largest AI investments, the share of entry-level workers increased by 1.15 percentage points compared to not-yet adopters, while low-intensity adopters slightly shrank their entry-level headcount share.

Sign up for our newsletter

Our weekly data driven newsletter provides in-depth analysis of workforce trends and news, delivered straight to your inbox!

Artificial intelligence has quickly become one of the most closely watched developments in the labor market. A growing body of research has examined which occupations are most exposed to AI and how workers use these tools on the job. Yet measuring AI adoption remains difficult. Most studies, including our own, rely on occupational exposure measures or measure adoption from job descriptions. Others rely on surveys. A more direct approach to measuring AI adoption is called for.

In joint research with Ramp, we can measure adoption directly by observing which companies purchase AI tools and invest in tokens. Ramp observes payments to AI vendors through corporate card and bill-pay transactions, allowing us to identify when companies begin making sustained investments in AI software. We link those spending records to Revelio Labs workforce data covering more than 21,000 US companies and examine how employment evolves around adoption. In this study, rather than estimating which companies are affected by AI, we examine changes in the workforce at companies that actually began spending to deploy AI tools.

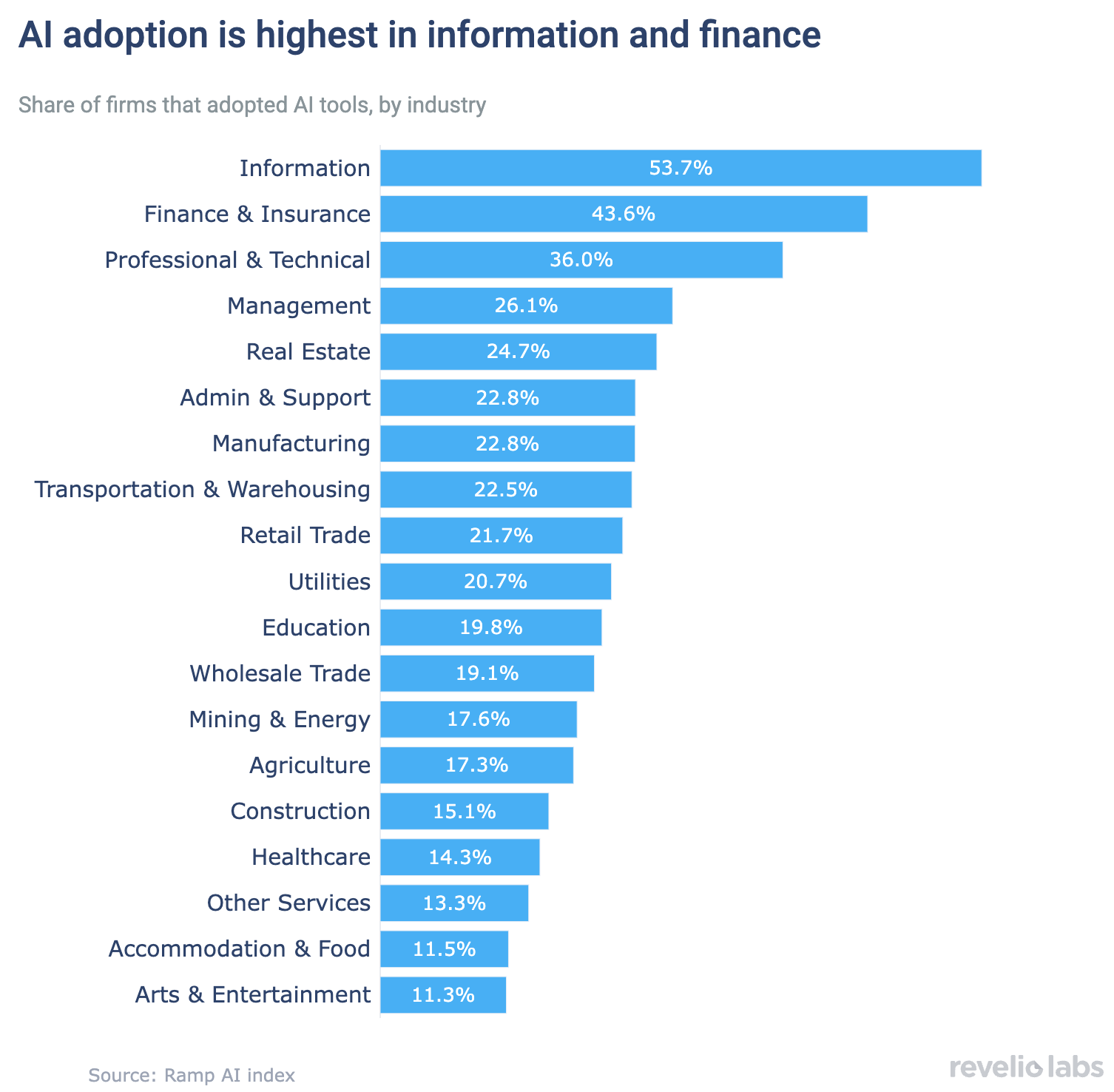

Which industries are adopting AI the fastest?

To measure AI adoption, we use Ramp transaction data to identify payments to AI vendors, including OpenAI, Anthropic, and other AI software providers. AI adoption is defined as the beginning of a sustained period of AI spending, requiring at least three consecutive months with at least $100 in monthly AI vendor purchases. This approach is designed to capture organization-level adoption rather than one-off experimentation. By this definition, roughly one quarter of companies in our sample had adopted AI by the end of 2025.

Adoption, however, was far from being evenly distributed across companies and industries. By the end of 2025, more than half of the Information industry companies in our sample had adopted AI tools. Adoption rates were also high in Finance & Insurance and Professional & Technical Services, while industries such as Healthcare, Construction, Accommodation & Food Services, and Arts & Entertainment lagged considerably behind.

This adoption and investment pattern is consistent with where generative AI currently delivers the most immediate value. Many early use cases involve writing, coding, research, analysis, and documentation—activities that are particularly common in knowledge-intensive industries.

How are AI adopters different from other companies?

Industry composition, however, is only part of the story. Companies that adopt AI differ substantially from companies that never do. Prior to adoption, adopters tend to be larger, faster-growing, more engineering-intensive, and more likely to be venture-backed. They also pay higher salaries and are disproportionately concentrated in technology-adjacent sectors.

For example, median year-over-year headcount growth is 6.0% among adopters, compared to 1.6% among companies that never adopt. Adopters are also more than three times as likely to be venture-backed and employ a substantially larger share of engineers.

These differences highlight an important challenge for measuring AI's impact. Companies that adopt AI are not a random sample of employers. Any attempt to measure the relationship between AI adoption and workforce outcomes must account for the fact that adopters were already different before adoption occurred.

How we compare adopters to not-yet adopters

A simple comparison between adopters and non-adopters would overstate the relationship between AI adoption and employment growth because adopters were already expanding more rapidly before adoption.

To address this challenge, we compare companies that have already adopted AI with companies that will adopt later but have not yet done so at a given point in time. Because adoption occurs at different dates across firms, this approach allows us to compare companies that are more similar in their characteristics and underlying growth trajectories.

We track workforce outcomes relative to the adoption date and compare them with those of companies that have not yet adopted. This research design allows us to estimate how employment evolves around AI adoption while avoiding many of the differences that separate adopters from companies that never adopt at all.

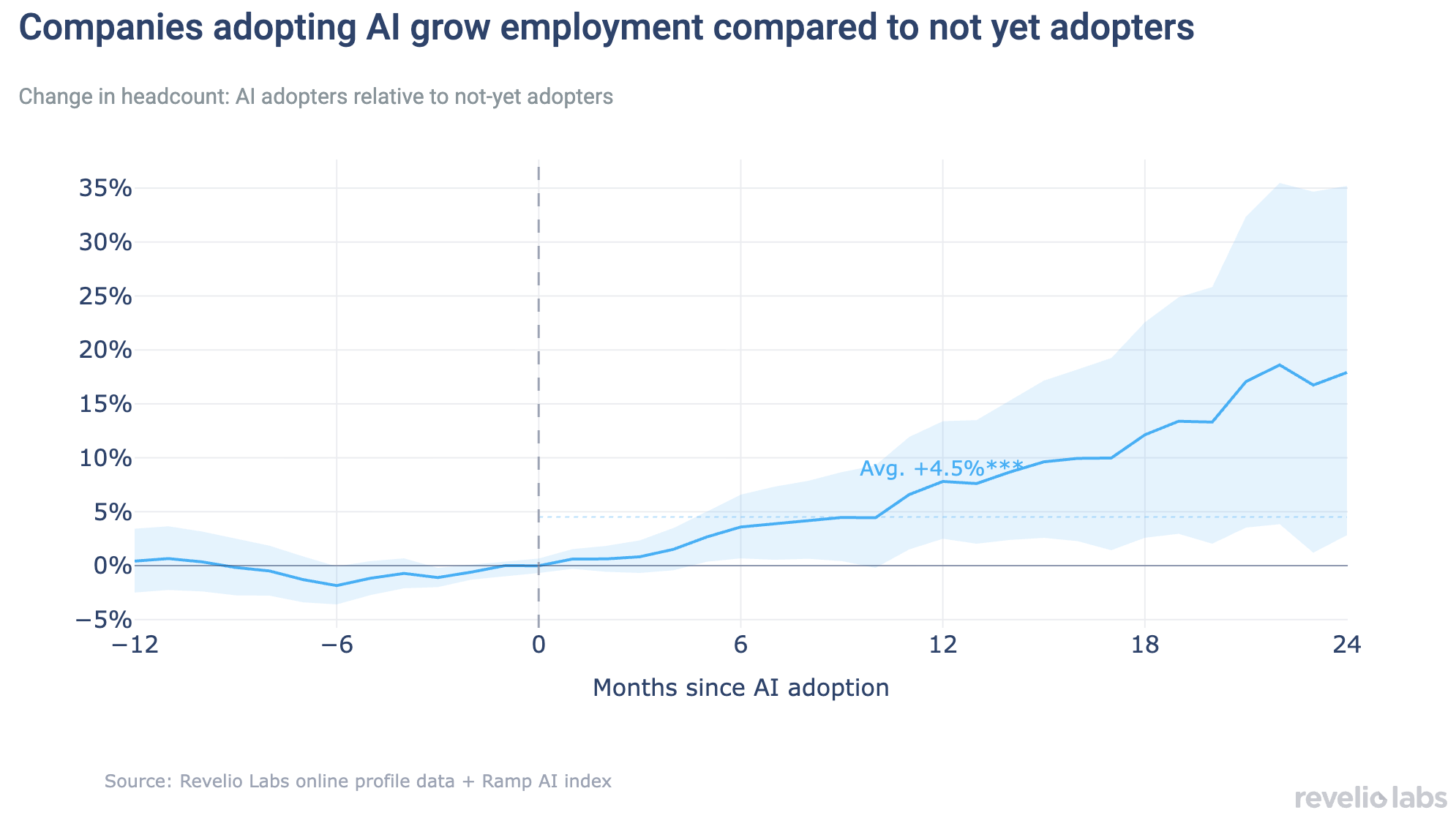

Do companies hire more after adopting AI?

Comparing companies that have adopted AI to otherwise similar companies that have not yet adopted, we find that AI adoption is associated with higher employment levels. Over the first 24 months following adoption, adopters maintain employment levels that are higher than companies that have not yet reached adoption. The event-study estimates show that these differences emerge gradually rather than immediately.

At face value, these results suggest that AI adoption is occurring alongside workforce expansion rather than workforce contraction. However, the average effect conceals substantial differences across adopters.

Do the biggest AI spenders hire the most?

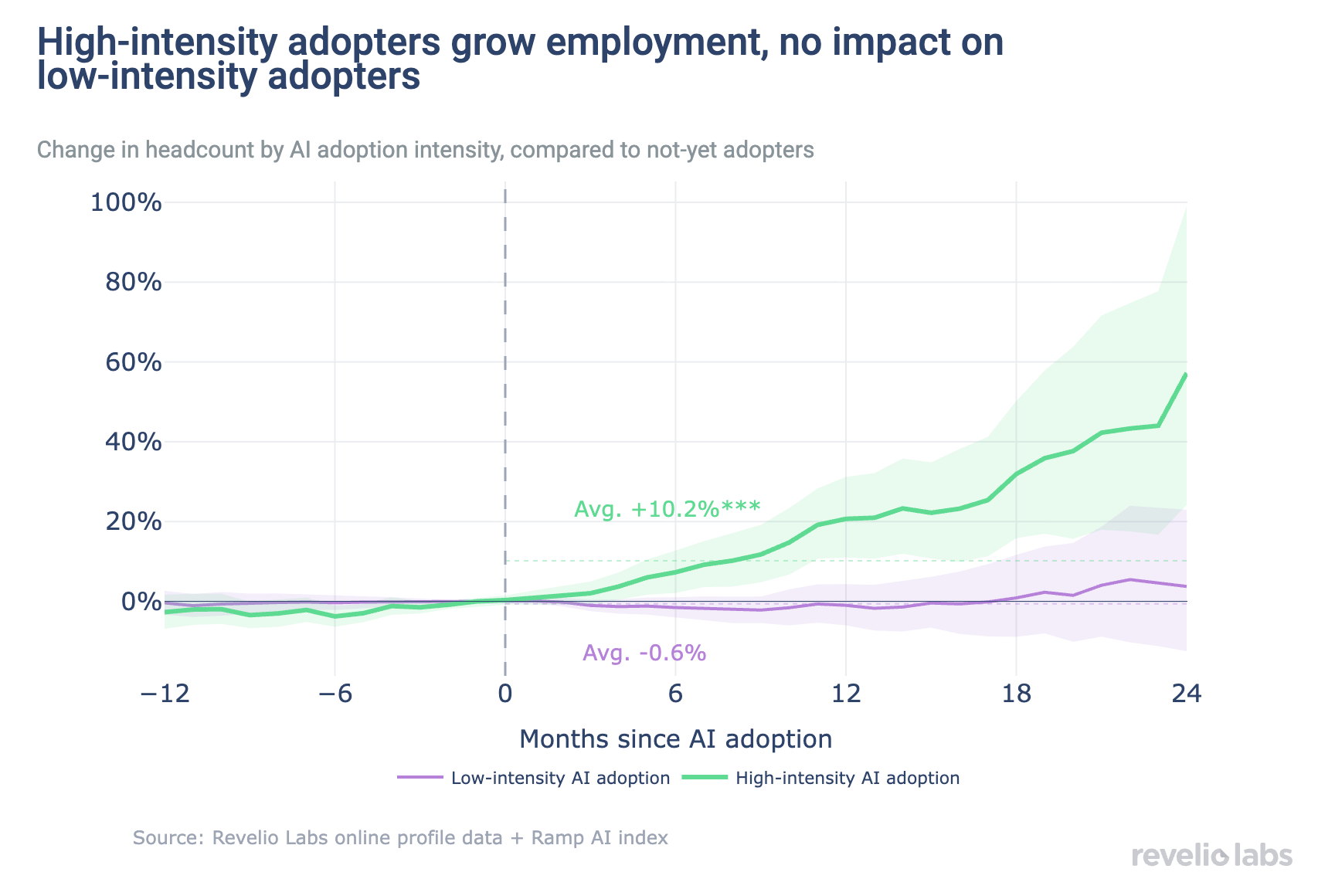

Not all companies adopt AI to the same degree. While some companies make relatively modest purchases of AI software, others make much larger investments and integrate AI more deeply into their operations.

To measure adoption intensity, we calculate AI spending per employee during the first three months following adoption. Companies in the top third of spending per employee are classified as high-intensity adopters, while the remaining companies are classified as low-intensity adopters.

The distinction is important. While AI adoption overall is associated with higher employment, the relationship is driven almost entirely by companies making the largest AI investments. High-intensity adopters maintain employment levels roughly 10.2% higher than companies that had not yet adopted AI, while low-intensity adopters show no statistically significant employment gains.

The timing of these effects is also notable. Employment trajectories remain similar around the adoption date and only begin to separate several months later, suggesting that any workforce effects emerge gradually as companies incorporate AI into their workflows rather than immediately after purchasing AI tools.

These results do not imply that AI mechanically creates jobs. Rather, they suggest that the companies making the deepest and most sustained AI investments are also the companies experiencing the strongest subsequent workforce growth.

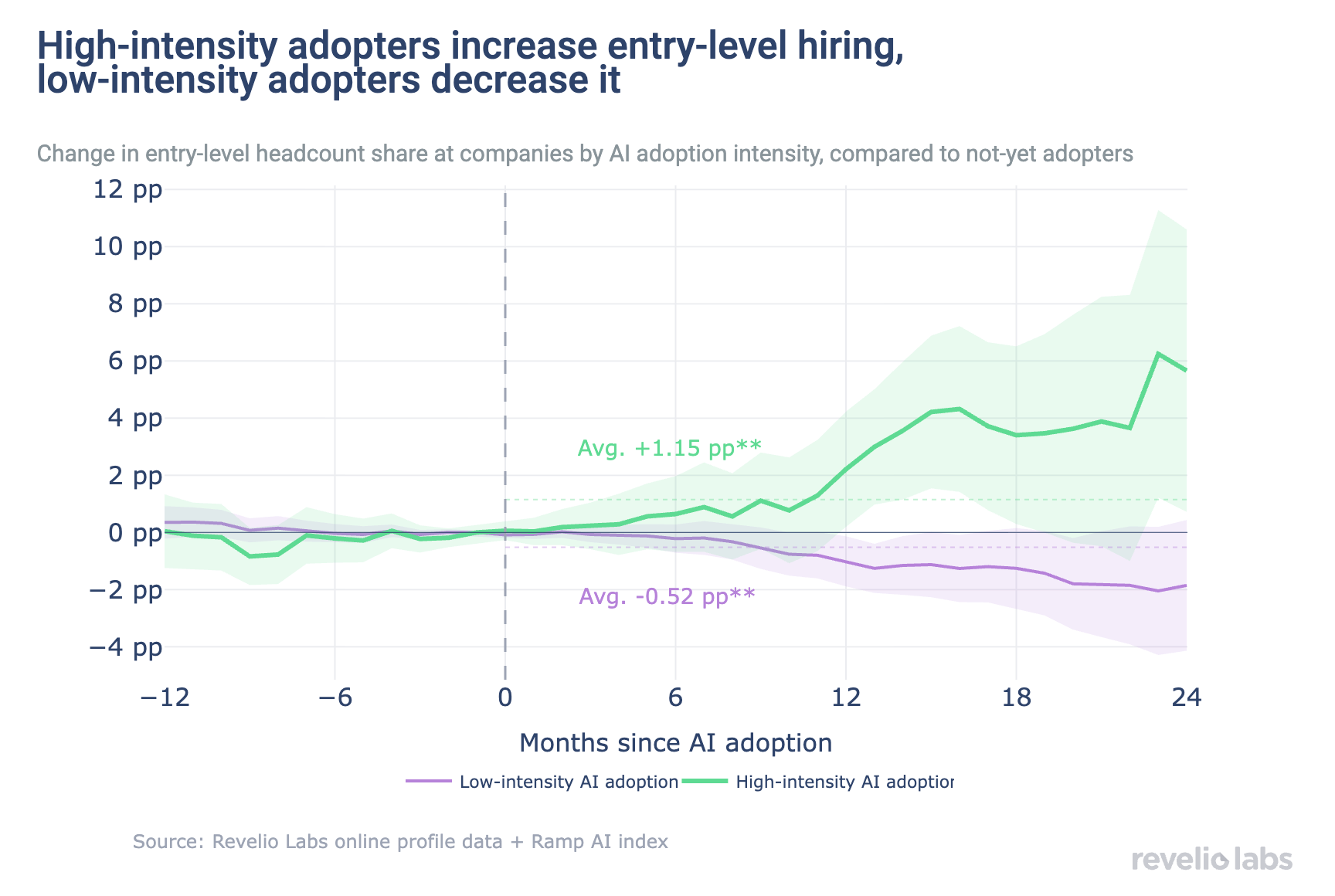

Is AI replacing entry-level jobs?

Much of the public discussion around AI focuses on entry-level work. Many tasks performed by junior employees—including research, drafting, documentation, and information gathering—are precisely the types of activities that generative AI systems can assist with. To examine whether adoption affects workers differently across seniority levels, we separately track entry-level and non-entry-level employment as classified by Revelio Labs’ seniority metric.

Looking at adopters compared to not yet adopters, we find little evidence that adopters are disproportionately reducing entry-level employment. Employment growth is similar for entry-level and non-entry-level workers, indicating that the overall gains are not driven solely by more senior hiring.

Differences emerge once companies are separated by adoption intensity. Among high-intensity adopters, the share of entry-level workers increased by 1.15 percentage points relative to companies that had not yet adopted AI. Low-intensity adopters move in the opposite direction, experiencing a modest decline in entry-level workforce share.

One interpretation is that companies making larger organizational investments in AI are using the technology differently than companies making smaller purchases. While both groups adopt AI tools, only high-intensity adopters show evidence of increasing the share of their workforce held by junior employees. Results in other studies (again, including some of our own work), are unable to distinguish between high-and low-intensity adopters, and may be picking up the signal from low-intensity adopters who seem to indeed be hiring fewer entry-level roles.

What does this mean for the AI labor market debate?

The debate around AI and employment often focuses on job displacement. Our results suggest a more nuanced picture.

AI adoption remains concentrated among a relatively narrow group of companies and industries. Adopters are disproportionately found in knowledge-intensive sectors and tend to be larger, faster-growing, and more technically oriented than companies that never adopt.

Within this group, AI adoption is associated with higher employment levels relative to companies that have not yet adopted. However, the relationship is highly uneven. Nearly all of the observed employment gains are concentrated among companies making the largest AI investments, while low-intensity adopters see little measurable change. High-intensity adopters also increase the share of entry-level workers in their workforce, suggesting that deeper organizational investments in AI are occurring alongside workforce expansion rather than contraction.

It remains too early to draw conclusions about the long-run effects of AI on the labor market. But the early evidence tells a different story: the companies spending the most on AI are, so far, the ones hiring the most.